Difference between Supply and Demand

Key Difference: In basic economics, supply is the amount of a certain products that the producer is willing and able to sell it at a certain price, if all other factors are constant. Demand is the principle that explains a consumer’s desire and willingness to purchase a certain good and the amount of money that they will spend on that product. Demand represents the quantity of the product or service that is desired by the buyers.

Supply and demand are basic concepts that are used in economics. These principles deal with the goods that are available in the market and affect the price of those goods. It is an important aspect of life that plays a big role in a person’s daily life, even if the person is not a student of economics.

In basic economics, supply is the amount of a certain products that the producer is willing and able to sell it at a certain price, if all other factors are constant. In layman’s terms, the price and the quantity a producer sets in order to sell his products is known as supply. The price of a product is most commonly determined by the supply and demand of the product. Ever notice, how shortages of certain products causes the price of the product to increase substantially? This is the lack of supply which causes the prices to rise.

In economics, the law of supply states that the higher the price of the product, the higher the supply of the product and lesser the quantity of the product, the higher the price of that product will be. This is due to the higher price creating more revenue for the producer, allowing him to produce more quantity. There are a certain number of factors that can affect the supply: the price of making the goods, the price of advertising, technology used to create the product, the number of raw materials required, availability of the raw materials, government regulations, taxes, etc.

Demand is the principle that explains a consumer’s desire and willingness to purchase a certain good and the amount of money that they will spend on that product. Demand represents the quantity of the product or service that is desired by the buyers. The demand relationship is the relationship between the price and the quantity of the product demanded. In layman’s terms, demand is the how many consumers are willing to purchase a product that is in the market and how much they are willing to pay for the product. A good example to explain this would be when you go clothes shopping, do you notice that discounts are given on the clothes from last season, well that is because the demand for last season clothes declines as it rises for this season’s clothes, causing the manufacturers to decrease the price in order to get rid of the old stock.

The law of demand states that consumers purchase more goods when the price is low and less when the price is high. The law says that the quantity demanded and the price of a commodity is inversely related, meaning higher demand-lower price and vice versa; but the catch is that all other factors must remain constant. There are a few exceptions to the law of demand such as Giffen goods, luxurious items and expectation of change in the price of commodity. Certain factors that affect demand are good's own price, price of alternatives available, price of related goods, personal disposable income, tastes or preferences and consumer expectations about future prices and income.

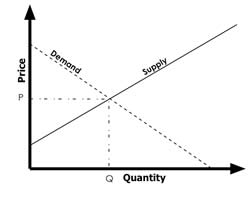

Most frequently, supply and demand go hand in hand. An increase or decrease in either one directly affects the other. There are four laws of the supply and demand model. They are: if demand increases and supply remains unchanged, then it leads to higher equilibrium price and higher quantity, if demand decreases and supply remains unchanged, then it leads to lower equilibrium price and lower quantity, if demand remains unchanged and supply increases, then it leads to lower equilibrium price and higher quantity and if demand remains unchanged and supply decreases, then it leads to higher equilibrium price and lower quantity.

Let’s look at it this way, if a producer of CDs produces 10 CDs to sell; now the people who wish to buy the CD are 20. This causes a shortage of CD, allowing the producers to increase the price of the CDs. But as the price rises, fewer people will opt to buy the CD, which will decrease the number of buyers for the CD. Now taking the same example into consideration, let’s change the number of the buyers, there are 10 CDs which were produced and there are only 5 buyers for the CD, the company will reduce the price of the remaining CDs in order to try and convince people to buy it.

|

|

Supply |

Demand |

|

Definition |

Supply is the amount of a product producers are willing and able to sell at a certain price. |

Demand is the consumer’s desire and willingness to pay for a price for a certain product or service. |

|

Background |

Supply is a basic principle that is used to determine the price of a product. It is most commonly used in economics. |

Demand is a principle that is also used to determine the price of the product based on the consumer’s desire. It is also most commonly seen in economics. |

|

Affecting factors |

Goods own price, price of related goods, technology used, price of inputs, expectations, number of suppliers and government policies and regulations. |

Good's own price, price of alternatives available, price of related goods, personal disposable income, tastes or preferences and consumer expectations about future prices and income. |

|

Law |

The law of supply states that the higher the price the higher the quantity supplied. This is because a higher price allows the supplier to get increased revenues, giving him capital to produce more. |

The law of demand states that if all other factors are constant, the higher the price of a good, the less demand it will have among people. |

|

Curve |

A basic supply curve is depicted as an upward slope. |

A basic demand curve is depicted as a downward slope |

|

Equation |

Qs = f(P; Prg S); P is the price of the good, Prg is the price of related goods and S is the number of producers. |

Qd = f(P; Prg, Y); Qd is quantity of a good demanded, P is the price of the good, Prg is the price of a related good, and Y is income. |

Image Courtesy: wikimedia.org

|

|

|

|

|

|

|

|

Comments

reyaz

Fri, 07/07/2017 - 16:49

Good ,tnx

Amir hamja

Tue, 06/10/2014 - 13:28

am very happy to here this kind of think

Abubakar tenimu...

Thu, 02/13/2014 - 11:17

Add new comment